You are viewing 1 of your 1 free articles

Impact of help to buy revealed

The government’s controversial help to buy scheme has been making waves since its launch in April 2013. So what impact has it really had on the housing market? Jules Birch crunches the numbers to find out

Help to buy is housing Marmite. For people struggling to get onto the housing ladder, not to mention house builders, estate agents, and coalition politicians, it tastes good. Great, even. But for economists and housing specialists it’s an acquired flavour at best.

Help to buy comes in two varieties. Part one is £6 billion worth of equity loans of up to 20 per cent of a property for buyers of new homes with a 5 per cent deposit. This started in April 2013 and was last month extended to run to the end of the decade.

Part two is £12 billion worth of mortgage guarantees enabling 95 per cent mortgages. It has been available to buyers of any home (new or old) since January 2014 and is due to run until December 2016.

Criticism of the first part of help to buy has been muted because it is directly linked to the supply of new homes. But the second part has proved far more controversial due to fears that it will boost demand, inflating a house price bubble that could burst leaving the taxpayer to pick up the tab.

Adam Posen, a former member of the Bank of England monetary policy committee, brands it ‘dysfunctional’, while even Liberal Democrat business secretary Vince Cable has called for it to be ‘reassessed’ in light of increasing house prices.

In contrast, prime minister David Cameron argues the scheme is helping thousands of people ‘realise their dream’ of homeownership.

In light of the controversy, are there actually measurable impacts on housing supply, mortgage lending, house prices and sales so far? And who is help to buy really helping?

Who’s been helped to buy so far?

Early government statistics do not support fears that it would be mostly well-heeled buyers of expensive homes in the south east that benefited from help to buy.

In the first nine months 14,823 equity loans were granted to buyers of new build homes with a mean price of £203,137 - well short of the maximum of £600,000. According to Downing Street, 89 per cent of these went to first-time buyers and 76 per cent were outside London and the south east. Similarly for the second part of the scheme, of the 2,572 mortgages guaranteed up to the end of January, 82 per cent went to first-time buyers and 85 per cent were outside London and the south east.

Greater regional distribution means the mean price of the homes involved was significantly lower at £148,048.

Who’s been priced out?

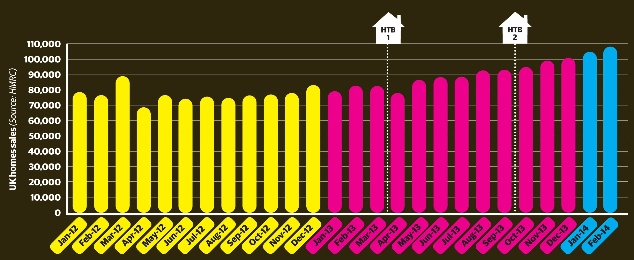

The impact on transactions

Monthly home sales collapsed from a peak of about 150,000 at the end of 2006 to around a third of that by the end of 2008. Sales recovered some ground in 2009 after interest rates were cut but ran at below 80,000 until the introduction of help to buy in March 2013.

A sustained recovery followed to 100,000 by the end of the year and 109,000 in February 2014, the highest monthly total since the end of 2007.

If you look at the 17,395 sales backed by help to buy in its first nine months, it’s hard to see how they alone can have had much influence on a UK market in which there have been 1.1 million transactions over the past year.

However, as Matthew Pointon, property economist at Capital Economics points out, the housing market works on confidence and on expectations that can become self-reinforcing. And if the second part of the scheme gets going to capacity it will add a much more significant 190,000 sales-a-year to the market.

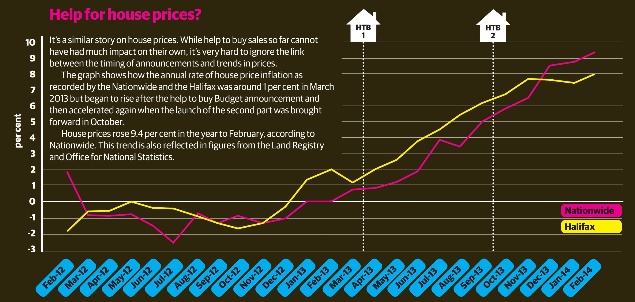

Help for house prices?

It’s a similar story on house prices. While help to buy sales so far cannot have had much impact on their own, it’s very hard to ignore the link between the timing of announcements and trends in prices.

The graph shows how the annual rate of house price inflation as recorded by the Nationwide and the Halifax was around 1 per cent in March 2013 but began to rise after the help to buy Budget announcement and then accelerated again when the launch of the second part was brought forward in October.

House prices rose 9.4 per cent in the year to February, according to Nationwide. This trend is also reflected in figures from the Land Registry and Office for National Statistics.

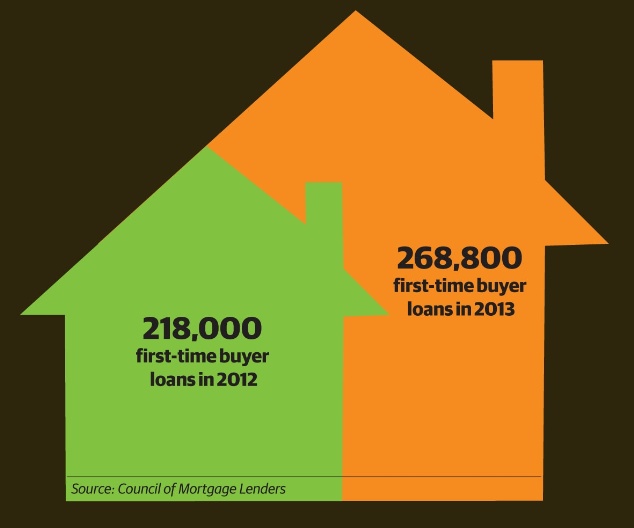

Help for the mortgage market?

The second part of help to buy offering lenders government guarantees has given banks the confidence to offer much higher loan-to-value mortgages.

First-time buyers have accounted for 88 per cent of the completions under both the first and second parts of the scheme so far. The diagram shows that members of the Council of Mortgage Lenders made 268,800 first-time buyer loans in 2013. That was a 23 per cent increase on 2012 and the highest annual total since 2007 though it is still well down on the early 2000s.

Seperately, figures from e.surv show that mortgage lending to high loan-to-value borrowers (more than 85 per cent) reached a six-year high in February and was up 74 per cent on a year ago, just before the launch of help to buy.

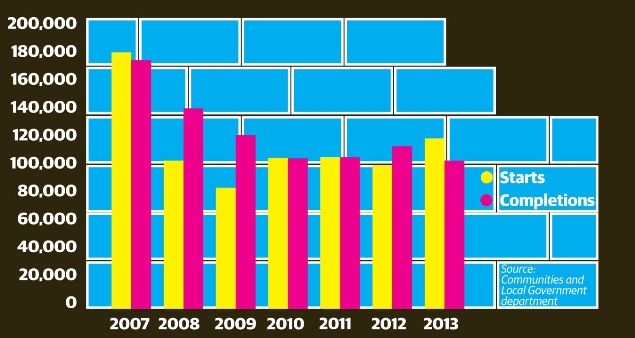

Help for house building?

Starts in 2013 were up 23 per cent on 2012 in England but are still down by half on pre-financial crash levels; and completions remain down on both 2012 and 2011.

Following the launch of help to buy in England in April 2013, starts increased from 27,870 in the first quarter of 2013 to 30,070 in Q2 and 32,520 in Q3 before slipping back slightly to 32,320 in Q4.

Increases have also been seen in planning applications and orders for new residential construction. The statistics so far show that, where help to buy accounts for only a small number of overall transactions, it is supporting a much more significant share of new build completions. The big unanswered question is how many new homes will be built because of help to buy and how many would have been built anyway.

Help for house builders?

In the year since help to buy launched in April 2013, Barratt shares have risen by around 60 per cent and Persimmon and Taylor Wimpey by 40 per cent.

Overall, their market capitalisations have risen by a cool £4 billion. Not bad given there are few strings attached in terms of increasing housing supply.

However, shareholders are not just benefiting from help to buy. After narrowly avoiding collapse during the financial crisis, house builders have slashed costs, and benefited from a range of other government subsidies and

removals of red tape - not to mention an improving economy. Shares in Barratt, for example, more than doubled in value in 2013 but they also doubled in 2012 and 2009.

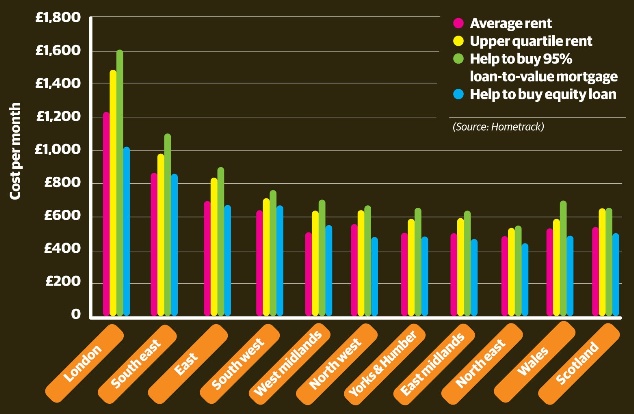

Is help to buy affordable?

How affordable are help to buy mortgages? The graph from housing market analyst Hometrack compares the cost of buying and renting a two-bedroom home.

Help to buy mortgage guarantees may make 95 per cent mortgages more available but the interest rate charged by lenders (around 5 per cent) is expensive. Costs are 30 per cent higher than average rents and higher even than upper quartile rents. Richard Donnell, director of research at Hometrack, believes this will limit its impact.

A help to buy equity loan looks cheap by comparison but borrowers are only buying 80 per cent of the home and will have to pay a fee for the equity loan after five years, raising concerns about long-term affordability.

According to the National Audit Office almost 30 per cent of households with equity loans owe more than five times their income, potentially causing problems if interest rates rise. And, given equity loans have to be repaid when homes are sold, there could also be a danger of people being trapped with insufficient equity to move.

Looking to the future

Help to buy alone cannot explain the upturn in the housing market over the last year - but government backing for the scheme has boosted confidence and created an expectation that prices will rise. What will happen next?

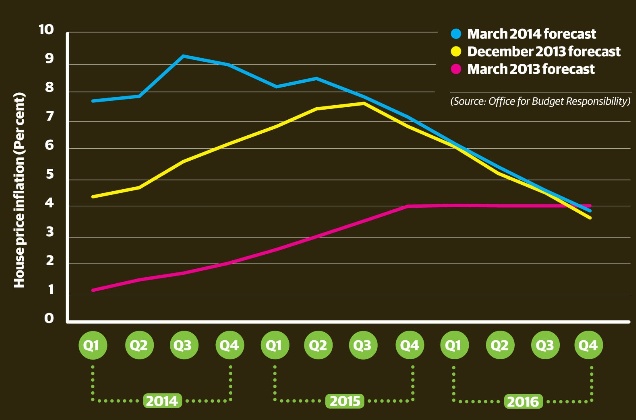

On house prices, the graph shows the independent Office for Budget Responsibility’s last three forecasts made in March 2013 (when help to buy was announced), December 2013 (the OBR’s first real chance to assess its impact) and March 2014 (after the extension of the equity loan part of the scheme). Priced Out estimates the forecast increase in prices in 2014 will mean that another 200,000 renters cannot afford to buy.

Note the expanding bulge for the period between 2014 and 2016. The OBR’s latest forecast amounts to a 30 per cent increase by 2018/19, which would leave house prices just 0.5 per cent below their pre-crisis peak in real terms.

In terms of supply, one of the most bullish predictions so far came from analysts at Morgan Stanley who forecast new housing starts could increase by 40 to 55 per cent by 2016 (on 2012 levels). This implies starts of between 140,000 and 155,000 by 2016; above the average seen since 1990 but still well below the 250,000 homes a year required to meet demand and help to bring house price inflation under control.