You are viewing 1 of your 1 free articles

Preparing for the future

Pete Apps has trawled through the financial statements of the biggest 75 housing associations in England, to reveal the key financial trends in the sector.

Video:

features code

Every year, the publication of housing associations’ global accounts is eagerly awaited by social landlords’ finance teams, lenders, government ministers and other general housing wonks.

The figures are typically published by the Homes and Communities Agency (HCA) in March, and provide the definitive statement on the sector’s finances. They are rigorously picked apart to provide crucial benchmarking data for associations’ relative performance.

This year, Inside Housing is jumping the gun. At a crucial moment for the social housing sector, as it faces down attacks on its financial performance from the prime minister and greater scrutiny than ever from the regulator, we have combed the financial statements of England’s 75 largest housing associations to provide the first baseline data indicating how the sector performed in the last financial year. (Scroll to the bottom of the page for an interactive table showing the full data.)

Video:

Ad slot

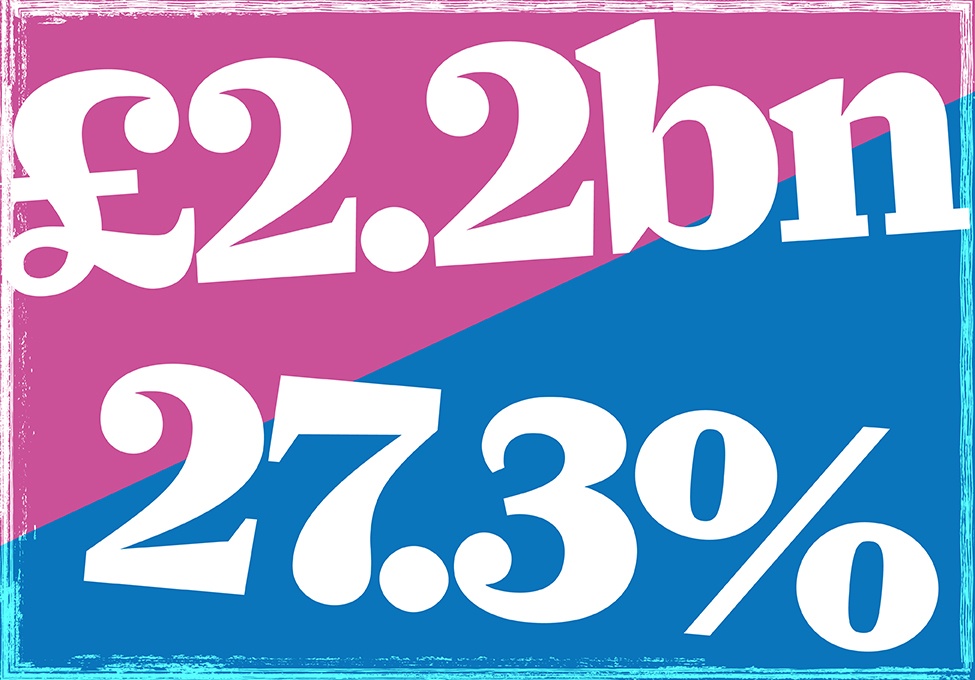

The numbers are encouraging – surpluses are up across the board from a combined £1.78bn to £2.2bn. And 57 of the 75 landlords brought in a bigger surplus year-on-year.

Pertinently, average operating margins have also increased – a 1.5% increase to 27.3%. Operating margin shows the percentage of turnover which was left after day-to-day costs are removed, and is a key measure of assessing financial performance.

In numbers

£2.2bn: combined surplus, up from £1.78bn last year

27.3%: average operating margin of the 75 largest housing associations

72.6%: percentage of sector’s income from core social lettings

£5.95bn: invested in building new homes

Future fit

This financial strength is particularly important as it will be severely tested in the years to come, with the sector required to find billions in savings to make up for chancellor George Osborne’s infamous rent cut - which means they will stop increasing rents by above inflation and instead reduce them by 1% annually for at least four years.

The accounts also show housing associations have used this strength to plunge just under £6bn into building new homes - a level of investment which could be threatened as the cuts bite.

Surpluses on the rise

In total, the biggest 75 landlords recorded a pre-tax surplus of £2.2bn. To compare, this is almost as much as the £2.4bn which was generated by all landlords last year, according to last year’s Homes and Communities Agency (HCA) figures. And it suggests a substantial rise is likely when the HCA publishes the next version of the global accounts in March.

It is an increase from last year of 19% for these 75 landlords. Digging into the accounts of these associations shows the cause is that turnover has risen 8.4% to £13bn from £11.9bn. Costs have risen too – but at a lower rate, from £8.8bn to £9.5bn. Landlords have also benefited from continuing low interest rates.

Turnover is up as a result of higher rents, which increased under the old rent formula of the Retail Price Index of inflation plus 0.5%, the conversion of properties from social to higher affordable rents and increasing diversification into market sale of housing.

This last factor means surpluses are largest in parts of the country where house prices are high – particularly London and the South East. In fact, all of our top 10 landlords with the biggest pre-tax surpluses are G15 members, with mammoth London landlord L&Q topping the list (see table: Largest housing association surpluses) with a record £209m surplus on a turnover of £624m.

David Montague, chief executive of 70,000-home L&Q and chair of the G15, says: “It reflects a combination of a focus on operating margin and measured risk taking – from both an L&Q perspective and a G15 perspective.”

Particularly in the current climate of budget cuts, housing associations are keen to ensure their surpluses are not misunderstood.

Anne Turner, chief operating officer at 38,000-home Orbit, which booked a £45.4m surplus in 2014/15, explains the surplus just looks at what is left after the costs of running the organisation and paying its debt are taken out. The cash does not then sit in a bank account - it is invested, often before the results are published, as capital expenditure to improve, buy and build homes.

“The first call on our profits is investment back into improving our existing stock,” she says. “Then we use it to fund development work so that we don’t have to borrow the entire cost of developing new homes.”

This year, housing associations put this financial muscle to work in a big way – investing £5.95bn in acquiring new homes from developers or building them, a substantial rise from £5.4bn last year (see table, page 29: Spend on development).

However, this level of investment may not last into the future, as associations grapple with the 1% rent cut, which will reduce turnover. Even if they make this up by diversifying further into the riskier sales markets, they may be inclined to keep more of their surplus in reserve.

As Mervyn Jones, director of the housing consultancy at Savills, says: “As associations move increasingly into supplying market homes, they have to have a model which is closer to house builders. That means keeping more of their surplus in reserve to protect against the market moving against you.”

Margin for error

The operating margin – which shows the percentage of landlords’ income left after costs – will come sharply into focus over the next few years as the rent cut bites.

This year it has increased across the top 75 – rising from 26.8% to 27.3%.

“An increase in operating margin of more than 1% is actually quite impressive,” says Mervyn Jones, director of Savills’ housing consultancy. “A lot of the big PLCs would be pretty happy if they were achieving that.”

Some housing associations put this down to a result of increasing movement into sales, as well as downward pressure on costs.

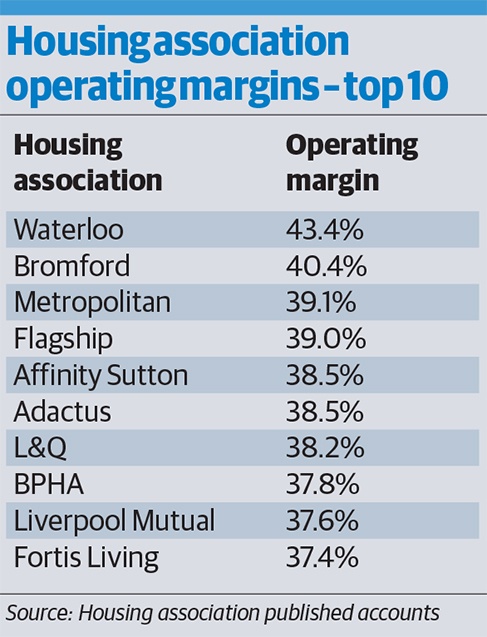

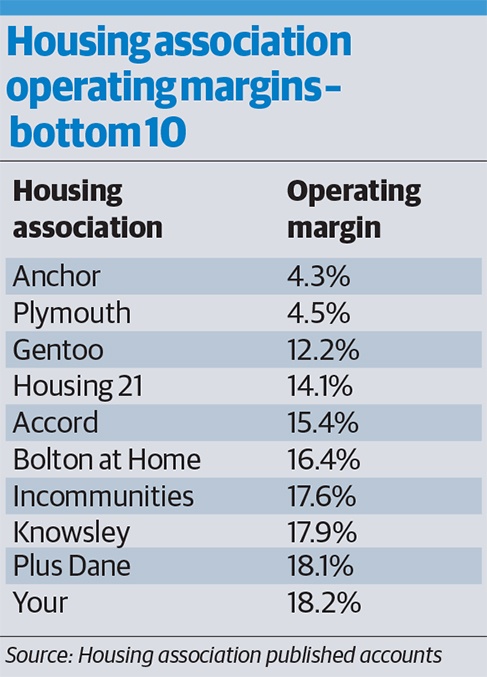

The combined accounts also show a huge level of variance across the country – with some organisations posting margins as low as 4%, and others pushing above 40%.

In both of the lowest operating margins there is a broader story to tell. Anchor, which has the lowest margin at 4.3%, is largely a residential care provider as well as a 27,000-home housing association - a business, by its nature, with much lower margins. The margin on its housing business is above 20% and much closer to the sector average, says chief executive Jane Ashcroft.

For 16,000-home Plymouth Community Homes, Nick Jackson, the director of business services and development finance, explains its 4.5%margin is a result of ploughing money into homes it took on from Plymouth Council after a stock transfer in 2009.

The low margin is partly a consequence of the significant work it has undertaken to improve the homes it took on, as well as the accounting treatment of funding it received under the transfer. Plymouth also has among the lowest rents in the country, and had expected to increase them under rent convergence, before it was scrapped in 2013. This leaves it needing to take £20m out of its business over four years to cope with the rent cut – but Mr Jackson says this can be achieved through a rigorous programme of efficiency savings to its cost base of just over £60m.

Many of the other housing associations with lower margins are stock transfer landlords in relatively low rent areas of the country – demonstrating that absorbing the rent cut will likely be more of a challenge for these landlords than others.

At the other end of the scale, the highest operating margin in the country belongs to Midlands-based Waterloo Housing Group, which finance direct David Pickering attributes to “a relentless focus on driving down costs over many years”. The 19,000-home landlord is putting this financial strength to good use – it surprised many in the sector by taking on the largest grant-funded programme in the sector under the 2015/18 Affordable Housing Programme to build more than 2,500 homes.

Promoting diversity

As Inside Housing revealed last month (‘A third plan no new sub-market rents deals’, 16 October), many landlords are looking to diversify their development plans over the next few years - building more for low-cost homeownership and market sale and less for social rent, as cuts bite and priorities for government grants shift.

This process has of course, been going on in the sector for many years, particularly since the grant reductions and the affordable rent regime introduced in 2011.

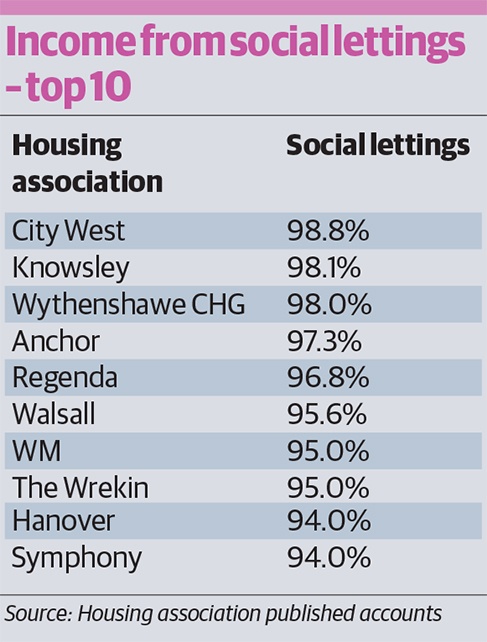

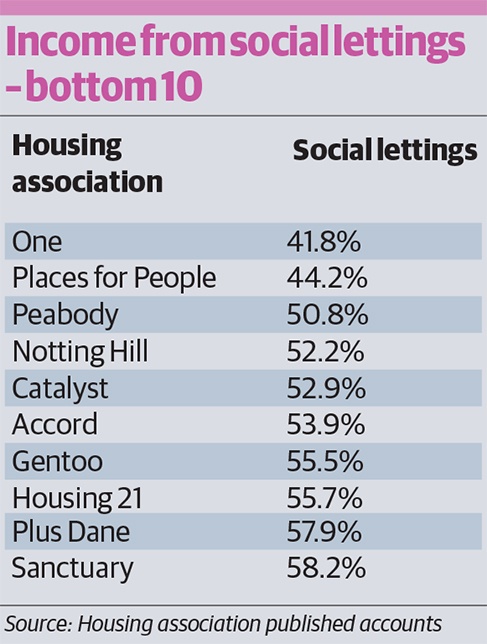

The combined accounts show this process has continued this year – with 72.6% of the sector’s income coming from core social lettings, against 75.2% in 2013/14. As with operating margin, there is evidence of wide differences across the sector – with City West Housing Trust in Salford deriving 98.9% of income from social lettings, compared to closer to 40% at the other end of the spectrum.

Those landlords which take virtually all their income coming from lettings are most exposed to the impact of the social rent cut, and are likely to begin diversifying in coming years to continue providing funds for sale.

Mervyn Jones, of Savills, says: “Associations which want to develop in the future, and all those I have spoken to say they do, are going to have to do market activity to pay for the development.”

This is a tougher challenge in the north of England, where the profits from selling homes are smaller and low property prices mean there is less demand for shared ownership.

As Gareth Swarbrick, chief executive of 13,700-home Rochdale Boroughwide Housing, says: “The current models of making up the cuts to grant from market sales don’t work in low value areas like Rochdale. It’s a challenge – and we’re going to have to be quite creative to find other ways of making it work.”

One Housing Group, based in London, made the lowest percentage of its income (41.8%) from core social lettings. This was largely a result of a hugely successful year for its sales programme which saw it turn over £78.7m from properties developed for outright sale.

Mick Sweeney, chief executive of the 15,000-home landlord, says: “Our overall approach is that two market sale homes can produce enough profit for one affordable home, if you don’t expect any grant.

“The results this year reflect the decision we took back in 2010/11 that we needed to make more from outright sale to carry on building affordable homes.”

Making it count

Earlier this year, Inside Housing’s development survey showed 2014/15 was a record-breaking year for new home building, and the scale of the financial investment in this development is made clear in the annual accounts.

Based on cash flow figures (which show all the money flowing in and out of the business each year), social landlords spent a mammoth £5.95bn on the acquisition and construction of new housing properties. Only 13% of this (£77m) came from government grant – the rest was money raised privately or investment of surpluses built up this year and in previous years.

The largest expenditure on development came from 98,900-home Sanctuary – which ploughed £328.6m into providing 3,154 new homes. The obvious warning to government is that it is this scale of investment it is putting at risk as it pushes ahead with cuts.

UPDATE: At 9.50am on 12.11.2015

The data table was updated to include a figure for the Wrekin Housing Trust’s development spend. This figure was not included in its published accounts, but was provided to Inside Housing after the article was published.