You are viewing 1 of your 1 free articles

Casting a shadow

As Universal Credit continues to be rolled out, Simon Brandon finds out how members of our welfare reform focus group are dealing with the changes

Video:

features style

It has been a pretty eventful year since Inside Housing last sounded out our 11*-landlord-strong welfare reform focus group.

“They aren’t getting enough to cover what they owe, let alone enough to get in front.”

Paul Malkin, income manager, Aspire

There was the small matter of a general election, one which delivered a Conservative majority government with a mandate to continue rolling out the changes to the benefits system begun previously under the coalition. And as the data from the focus group members shows, it’s not just the system that has been altered as a result; change has come to both housing providers and the lives of their tenants, too.

Perhaps the most significant adjustment has been the continued roll-out of Universal Credit (UC), which has been gathering steam after a slow start. As of September this year, according to government figures, 126,000 people now claim UC compared with 14,000 one year ago.

Video:

Ad slot

UC combines six separate benefits - including housing benefit - into one monthly payment. For social landlords and their tenants, the biggest implication promises to be the change in the way rent is paid.

Previously, as a stand-alone benefit, it was paid directly by the Department for Work and Pensions into providers’ bank accounts. UC is paid into claimants’ bank accounts, however, and they must take responsibility for paying their rent themselves (although vulnerable tenants, or those who have fallen into arrears, can apply for what’s called an Alternative Payment Arrangement - a reversion back to the old system, in effect, whereby rent is paid directly to landlords).

“We need to be proactive, which takes more resources, because we have to know everyone’s payment date and remind them separately before that.”

Lorraine Giddings, business change project manager, Salix Homes

So far, UC has been restricted to new claimants, or those with a change of circumstances. Someone losing their job, for example, would now apply for UC rather than Jobseeker’s Allowance.

The initial period between claim and payment takes around five weeks - and that has dropped some tenants straight into trouble (see box: A tenant’s perspective).

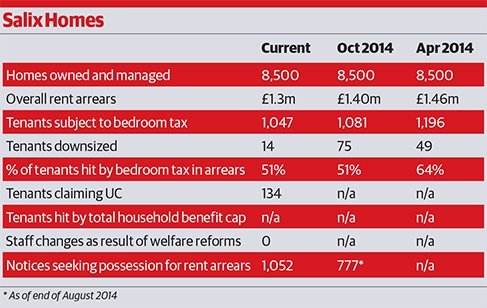

“Because there is an assessment period of five weeks, plus a seven-day waiting time, that’s where we’ve seen a lot of arrears coming from,” says Lorraine Giddings, business change project manager at 500-home Salix Homes, one member of our focus group. UC was rolled out to the Jobcentre in Salford - Salix’s area of operations - in December last year.

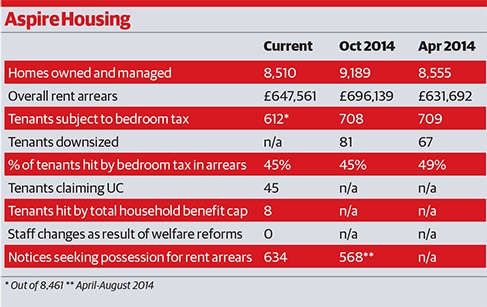

Elsewhere in the North West of England, 9,000-home Aspire Housing has been issuing food bank vouchers to tenants to help them cope with the shortfall before that first claim is paid.

“They aren’t getting enough to cover what they owe, let alone enough to get in front,” says Paul Malkin, income manager at Aspire.

Another difference from the housing benefit system to which landlords are having to adapt is the new payment schedule. “Whereas with housing benefit we would receive that for everyone [on the same day] every four weeks, with UC everyone’s payment date is different, so everyone’s arrears level will be different,” says Ms Giddings. “That is a risk, keeping on top of it. We need to be proactive, which takes more resources, because we have to know everyone’s payment date and remind them separately before that.”

But on the whole, she concludes, people are managing. “Some are struggling, as you would expect… but it’s interesting how many people are paying in full, and even clearing their arrears.”

Overall rent arrears

By and large, the changes to the welfare system have not had a major effect on arrears overall. “The overall trend is for arrears to be reducing,” says Debra Berry, head of housing and customer services at Aspire Housing, and she might as well be speaking for the majority of focus group members.

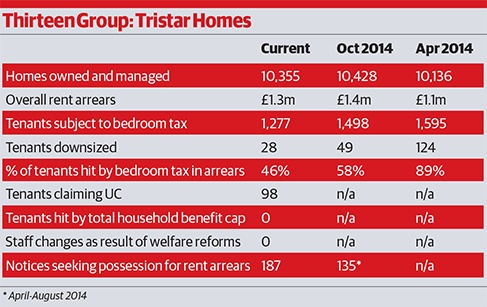

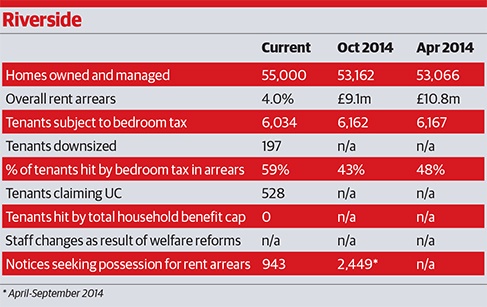

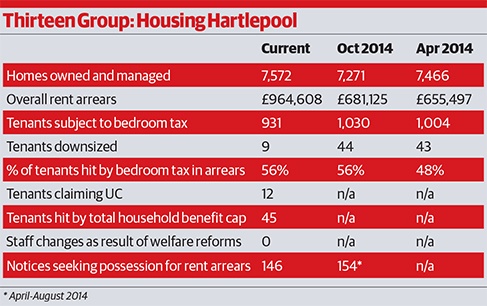

The one notable exception to the downward trend in arrears has been Housing Hartlepool, which has reported a leap in arrears of nearly 50%. But it hasn’t fazed the organisation too much, says Dave Pickard, group director of operations at Thirteen Group (of which two focus group members - Housing Hartlepool and Tristar - are subsidiaries).

“Last year, the local authority did start to pay some elements of the bedroom tax for customers in Hartlepool, but once that stopped, arrears shot up,” he says. “People had got used to the fact that the shortfall was being paid for them - and then it wasn’t. So there was a spike, but that has levelled off now.”

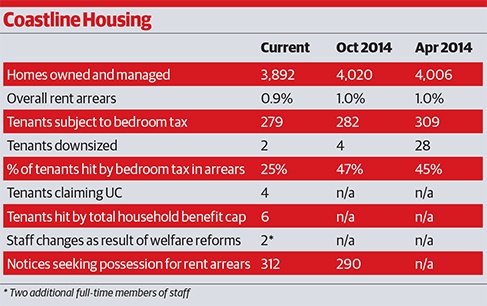

Down in Cornwall, however, one group member is not feeling positive about the future despite a steady reduction in overall arrears. “We have reduced rent arrears for the tenth year on the trot,” says Kevin Brown, head of housing services at Redruth-based Coastline Housing, which has 3,892 homes. “But our business plan assumes increasing rent arrears now.

“Families are being hit by benefit cuts and the increase in the cost of living… we won’t make it 12 years on the trot. We can’t possibly.”

Bedroom tax

There were plenty of gloomy prognoses before the introduction of the bedroom tax two-and-a-half years ago, too. Not all of them have been borne out.

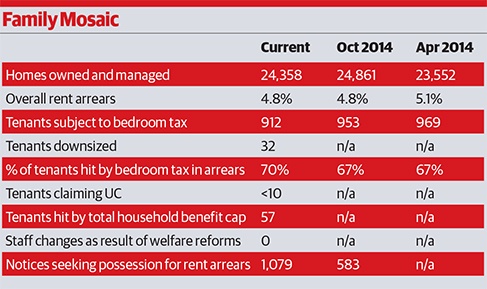

“Everyone said, ‘Woe are us, evictions are going to go through the roof.’ It didn’t happen, did it?” says Viv Davies, director of collections and credit control at 24,358-home Family Mosaic. “There was an initial spike [in arrears], and some are being camouflaged by discretionary housing payments, but those stories have fallen off. Actually the bedroom tax is boring now, isn’t it? Our total arrears are coming down, so for me it hasn’t had a huge effect.”

Enough time has passed since its introduction, says Mr Malkin of Aspire, that those initial reverberations have simply now been absorbed. “It has become the norm,” he says. “People are used to it. They just fall into our normal rent arrears process.”

One of the most easily identifiable trends among focus group members over the past few years has been the drop-off in the numbers of tenants downsizing as a result of the bedroom tax. That, says Ms Giddings, could be because the easy cases have already been dealt with.

“When the bedroom tax came in, we set up a dedicated team to focus on people who were under-occupying. They hit it hard and got a lot of results,” she explains. “So when it starts, you get a lot of the low-hanging fruit.”

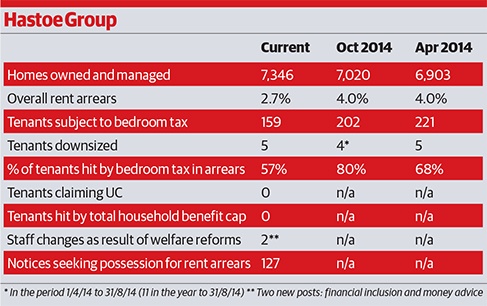

Mr Pickard says his organisation saw some evidence last year that the bedroom tax was still forcing tenants to move, but into the private rented sector rather than to another social rented property. From a business point of view, he says, this is a possible explanation for a small rise in tenancy terminations across the group. Thirteen Group’s response since April this year has been to cover either all or half of the bedroom tax shortfall in a few areas, but with caveats for the affected tenants.

“If you were in arrears, you have to make an agreement to pay them back and stick to it; you have to let us in first time for gas servicing; and you have to behave yourselves. No anti-social behaviour,” Mr Pickard explains. “We are going to do a full evaluation in six months. What really makes the business case for this scheme is the fact it anchors people in their tenancies. If we can avoid tenancy failure and avoid costs coming at us as a result, then the money we put into this could be offset… The early signs are quite promising.”

New staff

Three focus group members have reported hiring extra staff to help cope with the ongoing changes, mostly in their money advice and income management teams. The former have been crucial in enabling landlords to be proactive about the impending mass switchover to UC through identifying the tenants most likely to be negatively affected and offering them support and advice early.

Caerphilly-based 4,927-home United Welsh has brought a new money advisor on board and has trained half its neighbourhood officers to offer money advice, too.

Part of the reason for that, says Lynda Sagona, United Welsh’s director of housing and communities, is to forge better relationships with tenants: “What we know now is that if tenants get to know our staff, they will get confidence in that relationship - and then if times get difficult, hopefully they will feel more able to pick up the phone [to us] and have that conversation.”

Other members haven’t hired new staff but are instead looking at new, more efficient ways of working. One result of Family Mosaic joining the Rental Exchange - a scheme set up by credit risk analysts Experian that enables the timely payment of social rents to count towards a positive credit score, in the same way as mortgage payments - has been an ability to categorise tenants in terms of their financial vulnerability, says Mr Davies.

“We are able to make use of other kinds of [anonymised] data [held on our tenants by Experian] such as from mobile phone companies and banks… to profile our tenants into high, medium and low risk,” he explains. This enables Family Mosaic to target its advice and support to those tenants most in need.

Household benefit cap

The household benefit cap, introduced in April 2013, continues to affect only a small number of tenants across focus group members. In July this year, the government announced a further reduction - from £500 a week for single-parent families and couples with children, and £350 a week for single people, to £442 and £296 a week respectively for households in London, and £358 and £258 for those outside the capital - which will take effect in April next year.

“We have identified those households who might potentially be affected by the benefit cap, and our approach has been very similar to when the bedroom tax came in,” says Mr Pickard. “We are out there on the doorstep, providing people with support and advice. If they are impacted and there is a loss of income, the financial inclusion team will find a way of managing a reduced income for their household.”

What happens next

So what does the future hold? Some members predict a rise in arrears: “The next couple of years are going to be tough,” says Mr Pickard. “We are making provisions for increased amounts of debt.”

Others can see a silver lining. For Ms Giddings, the increased contact with tenants that the roll-out of direct rent payments under UC will necessitate is a good thing.

“The people who pay their rent on time, maybe report the odd repair - they carry on under the radar,” she explains. “This is a really good opportunity to get to know our customers better. We are trying to see it as an opportunity.”

We will know more in a year’s time. There are plenty of changes yet to come, not least the roll-out of UC across the board - but, as Mr Davies puts it: “Tenants are more resilient than people give them credit for.”

* Link Group was not able to participate in the welfare reform focus group for this check-in, due to staff illness.

A tenant’s perspective

Ann-Marie Young, 45, a tenant of Coastline Housing from Redruth in Cornwall, lost her job earlier this year and immediately applied for Universal Credit.

The online application, she says, was “easy enough”, but her subsequent experience of the scheme - beginning with an appointment at her local Jobcentre - didn’t go as smoothly.

“I think because it’s new in this area, the [Jobcentre] staff didn’t know what they were talking about,” she says. “‘Phone the number on the piece of paper.’ That’s all I got told. Things weren’t explained very well.”

Ms Young was told to expect her first payment in five weeks, only to be told - five days before the end of that period - that she wouldn’t receive any benefits after all because she had been paid for her last month at work.

“I had no money at all to pay my council tax, my rent, or to live on,” she says.

While working, Ms Young had been paying her rent herself, but the delay meant she fell immediately into arrears.

“You have to inform your landlord and council tax people you’ve lost your job,” she says. “When I contacted Coastline, they said OK, but there was a lot of pressure. Every week you get a letter demanding your rent. You feel like nobody is listening to you because you have to keep phoning up to explain your situation.”

In the end, Ms Young felt she had no choice but to raid her life savings to make sure she was up-to-date.

“I was lucky to get a job and get back to work, because I hate to think what sort of state I would have been in otherwise,” she says.

Related stories